Stablecoins have had a remarkable few years.

Not long ago they were treated as a niche crypto instrument: useful for trading, maybe remittances, mostly speculation-adjacent. Today, especially since 2025, they’re increasingly regulated, integrated into real financial infrastructure, and used as legitimate settlement tools by established industry giants. They move at internet speed, settle 24/7, and they don’t care what country you’re in.

And yet, at checkout, they’re still rare.

According to research by Boston Consulting Group (BCG), stablecoins process more than $62 trillion in annual transfers, but only about $350–550 billion (less than 1%) of that represents payments for goods and services. Even though that segment is reportedly growing at roughly 50% annually, it remains a small fraction of total volume.

So if stablecoins are faster and cheaper, why aren’t they already a default way to pay online and at the terminals? Because the real challenge isn’t the rails. It’s in the last mile.

Stablecoins settle efficiently on-chain. But commerce doesn’t happen “on-chain.” It happens in POS systems, reconciliation dashboards, refund workflows, and customer support tickets. For stablecoins to scale, the stablecoin layer must disappear into the background for both the merchant and the consumer.

A Tale of Two Sides

Payment systems are classic two-sided platforms. They enable interactions between two endpoints: Merchants and consumers. In this ecosystem, the value unit isn’t the currency; it’s the transaction.

The ultimate goal of any payment system is simple: ensure transactions can flow smoothly from the consumers to the merchants. The specific rails are secondary. It’s like delivering a package; as long as it arrives safely and on time, it doesn’t matter whether it came by plane or by train.

This is where crypto-native players often miss the forest for the trees: Stablecoins are not the product. The payment is the product.

If stablecoin payments are going to scale, merchants can’t be forced to become crypto companies, and consumers shouldn’t feel like they are performing a technical workaround.

Merchants: Look Ma, No Cryptos!

Most merchants don’t wake up excited to adopt a new technology. They wake up (often at night) thinking about inventory, staffing, margins, and customer retention.

When stablecoins enter the conversation, the merchant’s reaction is purely practical. Even if they acknowledge that stablecoins offer lower fees and faster settlement, they also know that the true cost of payments lives in daily operations, not the line item for processing fees. New technology introduces new unknowns, and merchants are not in the business of collecting unknowns.

The merchant’s question is simple: How do I accept stablecoins without turning my business into a crypto operations team?

A successful ecosystem must allow stablecoins stay out of the merchant’s way as much as possible. While a consumer might use crypto knowledge to initiate a payment, the merchant’s experience (beyond the POS or the payment gateway (PG)) should remain virtually unchanged. The goal isn’t to rebuild commerce around crypto; It’s to plug stablecoins into the systems that already run the business: order management, POS, customer support, settlement, reconciliation, and reporting.

Furthermore, merchants have no desire to expand their regulatory surface area. If accepting stablecoins means monitoring wallet histories or worrying about cross-chain sanctions exposure, adoption dies on arrival.

The solution is straightforward: convert to fiat early. By off-ramping to familiar currencies upstream in the value chain, merchants can focus on what they do best, making products and serving customers, rather than worrying if the USDC they just received is clean.

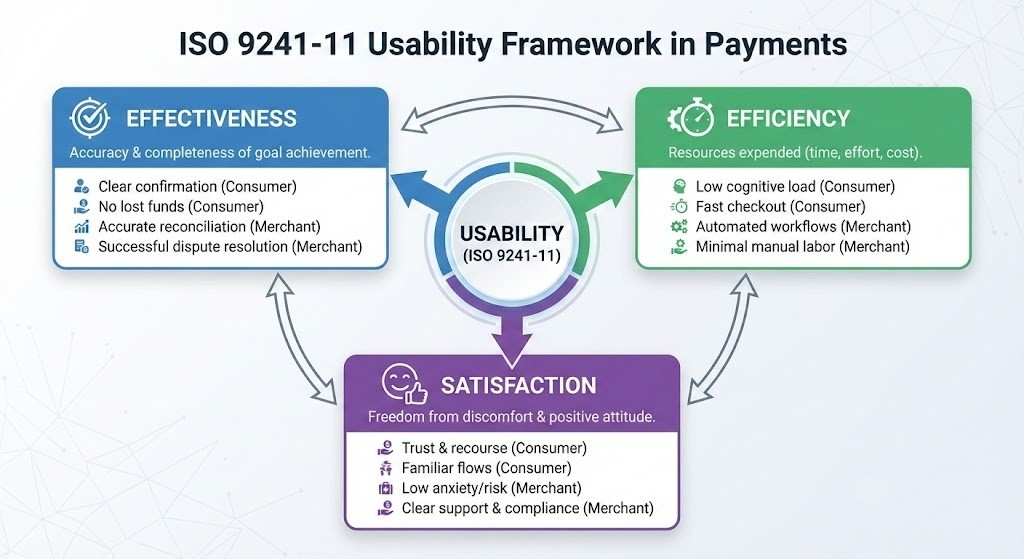

Consumers: effectiveness, efficiency and satisfaction

Consumers have a different set of priorities. They don’t care about operations or compliance. They judge a payment method by its usability. Subconsciously, they benchmark every transaction against the ISO 9241-11 usability framework, which defines usability through three distinct pillars:

Effectiveness: Can the goal be achieved accurately and completely? The payment must confirm clearly, settle quickly, and fail predictably. If a transaction gets stuck or isn’t recognized by the merchant, the technical elegance of the blockchain is irrelevant. Without instant confirmation, a consumer might fear the payment failed and unintentionally double-pay. An effective system minimizes "negative consequences" (Bevan et al. 2016), such as the irreversible loss of funds from sending to a wrong address.

Efficiency: What resources (time, effort, cost) were required to get there? Stablecoins should have the advantage here, but in practice, they often feel slower. A credit card checkout takes seconds: details autofill, fees are invisible, and the merchant absorbs the cost. With stablecoins, a user may have to open a separate wallet, select a chain, confirm the token, and pay a gas fee. If the merchant only supports one network, the user might even need to bridge funds, adding layers of complexity that kill the "efficiency" of the tech.

Satisfaction: Is the experience free from discomfort, and what is the attitude toward the product? Satisfaction is about trust and recourse. If the user journey feels "alien", riddled with cryptic errors or inconsistent flows, the consumer will retreat to what they know. If frontline sales and support staff aren’t trained (e.g., “We accept stablecoins but not that USDC”), the friction creates a lack of confidence that prevents repeat usage.

Incentives also play a massive role. Credit cards offer rewards, fraud protection, and "buy now, pay later" features. Consumers have been trained for decades to expect a "kickback" for spending. In the current stablecoin landscape, the consumer often sees only the downsides (effort and network fees) while the benefits remain invisible.

Perception matters as much as, if not often more than, reality.

What’s in Your Wallet?

Every new payment method is judged against the one someone reaches for without thinking. That "default" is the invisible benchmark stablecoins are competing against. For many consumers, that default is a credit card, either as a physical card or provisioned into a digital wallet. In some markets, it might be a super app or a national payment rail.

Most consumers don't care about the rails; they care about the moment of purchase. Did it go through? Was it easy? If I get scammed, can I get my money back? This is why first-in-wallet status is so powerful. It isn’t just a preference; it’s a habit reinforced by years of consistent experience.

Look at the history of credit cards. Diners Club didn’t win by trying to replace cash everywhere overnight. It started by solving a narrow problem in travel and dining, where merchants didn't trust out-of-town checks and consumers didn't want to carry stacks of bills. It created just enough acceptance to become useful, and just enough usefulness to become familiar.

Eventually, familiarity turned into trust, and trust turned into habit, triggering the “cross-side” network effect: more merchants accepted cards because consumers had them, and more consumers carried cards because merchants accepted them.

Stablecoins face this same structural climb. They aren’t competing against no payment; they are competing against defaults that have had decades to become invisible.

This is why the path forward likely doesn't start with replacing the first slot in the wallet. It starts with earning the second. This is the structural truth of the payment gap.

In the next issue: we’ll look at where stablecoins are most likely to win that second position, and why that matters far more than trying to go head-to-head with card networks on their strongest ground.

References and Sources:

BCG. Stablecoin Payments: The Truth Behind the Numbers. 2026.

.png)