How cross-border business settlement is driving Africa’s digital payment transformation

Africa’s payments story is often told through the lens of consumer adoption: mobile money success, fintech diffusion, remittance growth, and financial inclusion. These themes matter, and they have shaped a generation of innovation across the continent. But they overshadow a more significant and less discussed development, one that is transforming commerce at the operational core of African economies.

Across sectors and markets, African businesses are adopting stablecoins to solve cross-border settlement frictions that have constrained continental trade for decades. This shift is not ideological or speculative. It is a pragmatic response to longstanding structural inefficiencies in regional payment infrastructure. And while the retail crypto narrative tends to dominate headlines, the stablecoin-led modernization of B2B settlement may ultimately prove far more consequential for Africa’s economic trajectory.

Stablecoins are not replacing local currencies or bypassing banks. Instead, they are providing a neutral, efficient settlement layer that allows African businesses to transact with one another and with global partners without the delays, costs, and FX exposures embedded in traditional systems. The continent’s digital payment transformation is being built not from the “last mile” up, but from the enterprise layer outward.

The Barbell Opportunity

Africa represents a unique opportunity in global payments, pairing extraordinary potential with equally significant structural frictions.

On one side of the barbell is economic promise. Africa has the world’s youngest population, with more than 60 percent under age 25. Mobile penetration exceeds 80 percent across major markets. Entrepreneurial culture is strong, and the demand for efficient financial services is expanding rapidly. Fintech and cryptocurrency adoption rates in Nigeria, Kenya, Egypt, and South Africa rival those of the most digitally advanced economies. Relatively smaller West African countries such as Senegal and Côte d'Ivoire are seeing remarkable growth in cryptocurrency usage, with market size increasing at double-digit rates.

On the other side lies a complex monetary landscape. Africa is not a single market; it is 54 sovereign nations, dozens of currencies, multiple regional monetary unions, and varying degrees of capital account convertibility. The result is a high-friction environment for cross-border business transactions.

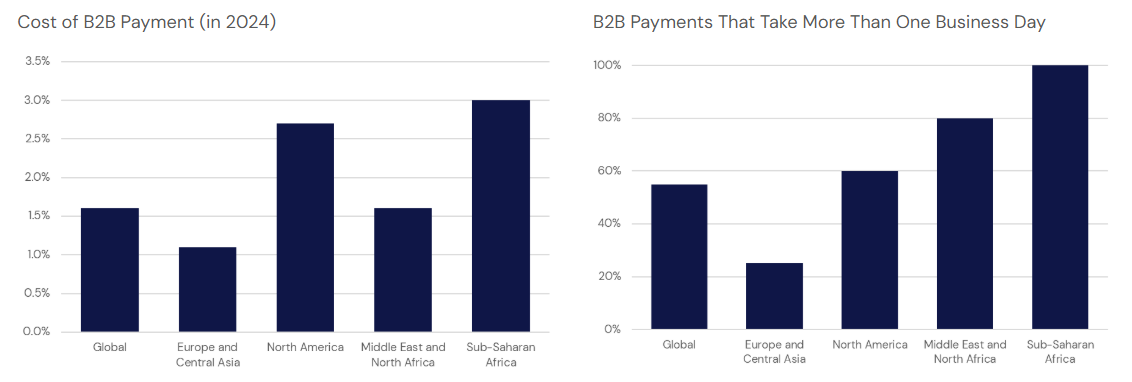

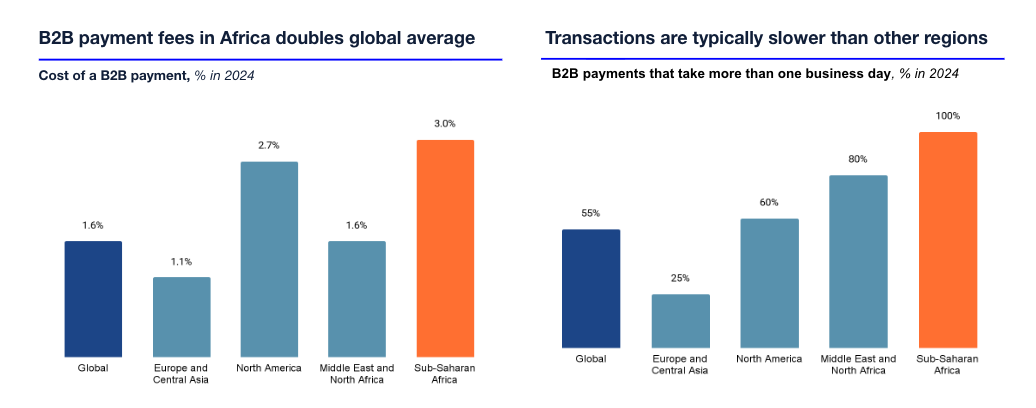

According to the Financial Stability Board (FSB), Sub-Saharan Africa lags globally in payment speed and cost. All B2B transactions originating from the region take more than one business day to process (versus a global average of 55% processed within a day), and each payment incurs fees of about 3%, almost twice the global average of 1.6%.

A business in Lagos cannot simply pay a supplier in Nairobi using naira and shillings. The transaction typically routes through USD or EUR, requiring two FX conversions, two fee events, settlement across correspondent banking networks, and exposure to multiple currencies over a multi-day period. According to data from the African Development Bank (ADB), over 80% of African cross-border payment transactions originating from African banks had to be routed offshore for clearing and settlement by banks abroad.

This fragmentation is not unique to Africa, but its scale is unmatched. For businesses operating across borders, it leads to:

- higher working capital requirements

- extended accounts receivable and payable cycles

- complex treasury processes

- inconsistent access to hard currency

- reduced operational efficiency

These frictions accumulate across supply chains, eating into margins and limiting the growth of small and medium-sized enterprises, which form the backbone of most African economies.

The Settlement Challenge

The challenges become clear when considering a simple commercial transaction. Imagine a Kenyan agricultural exporter selling to a Nigerian food processor.

Under the existing system:

- The Kenyan exporter invoices in foreign currencies, typically USD or EUR.

- The buyer must convert naira (NGN) to USD or EUR.

- Funds move through correspondent banks (often offshore).

- The exporter converts USD or EUR back into Kenyan shillings (KES).

- Settlement typically takes 4–6 business days, or more.

During this period:

- The exporter bears shilling volatility.

- The importer bears naira volatility.

- Both face conversion spreads and transfer fees.

Neither party is trying to take currency risk. Yet both must manage it as a byproduct of simply doing business.

Multiply this across hundreds of partners in multiple markets, and the picture becomes clear: African businesses and the global enterprises who work across many countries on the continent are not just managing supply chains; they are managing volatile FX portfolios. The complexity is substantial, and the operational burden falls disproportionately on SMEs with limited treasury resources.

Why Stablecoins Fit Naturally

Stablecoins offer a faster, cleaner, and more predictable settlement mechanism, and in the B2B context they function not as replacements for local currencies but as operational tools that sit alongside existing treasury practices.

Their fit in African markets stems from several reinforcing dynamics. Most African corporations already maintain USD positions for trade finance, procurement, and inventory management, which makes a USD-denominated stablecoin feel less like a new asset and more like a digital extension of instruments they already use. This familiarity pairs naturally with the practical advantages: settlement windows that shrink from days to minutes, improvements in working capital forecasting, and the elimination of multi-step FX conversions that typically introduce both cost and pricing uncertainty.

Stablecoin rails also reduce the layers of intermediaries (multiple PSPs, correspondent banks, and cross-border processors) that businesses currently rely on, simplifying payment operations and minimizing reconciliation risk.

Africa’s financial infrastructure is already mobile-first, with businesses accustomed to digital interfaces through mobile money platforms, stablecoin settlement represents a logical evolution rather than a wholesale shift in behavior.

In Aquanow’s experience working with financial institutions globally, the most durable and successful stablecoin implementations are the ones that address concrete operational bottlenecks. Africa’s cross-border B2B settlement challenges align almost perfectly with this pattern.

The B2B Advantage

While consumer applications tend to dominate public narratives around digital assets, the business-to-business segment is emerging as the more natural early adopter of stablecoin infrastructure. The logic is straightforward: B2B transactions involve larger values and higher operational stakes, where even small percentage improvements in cost or settlement time translate into meaningful financial gains.

Corporate treasury teams also have a deep understanding of settlement risk as they see firsthand the impact of delayed payments, currency exposure, and reconciliation complexity, and they are explicitly mandated to optimize these processes.

From a regulatory standpoint, B2B adoption generally encounters fewer sensitivities than consumer-facing activity. Retail crypto usage raises questions about monetary sovereignty and financial inclusion, whereas stablecoin-based business settlement does not alter domestic monetary dynamics; it simply makes cross-border commerce more efficient. This alignment tends to invite less regulatory friction.

Perhaps most importantly, the working capital benefits are both clear and immediate. Compressing accounts receivable and payable cycles from days to minutes improves liquidity, strengthens inventory management, and enhances cash conversion cycles—advantages that resonate strongly with enterprises across the continent.

Immediate operational use cases

We are already seeing stablecoins used for:

- commodity and raw material trade

- manufacturing supply chains

- logistics and procurement

- professional services

- cross-border contract settlement

These developments remain largely absent from public narratives but are growing rapidly in practice.

Operational Impact: More Than Speed

The impact of stablecoin settlement extends well beyond faster payments. Blockchain financial rails offer a series of operational improvements that enhance efficiency without altering the role of banks in the financial system.

By enabling businesses to settle cross-border obligations in a single digital format, stablecoins reduce the need for companies to maintain multiple foreign banking relationships solely for transactional purposes, easing administrative and compliance burdens while keeping core banking partnerships intact.

They also simplify payment operations by reducing reliance on a patchwork of payment service providers, each with their own cut-off times, fee structures, and settlement processes, allowing firms to centralize more activity within a unified digital asset framework.

The transparency of blockchain-based settlement provides real-time visibility into payment status, improving forecasting and cash management for treasury teams who often operate with limited information in traditional correspondent banking networks.

Finally, a shorter list of intermediaries required to facilitate each leg of a transaction means businesses face lower operational risk as they curtail potential failure points, expose themselves to fewer reconciliation challenges, and minimize delays.

Taken together, these improvements help firms operate more efficiently and resiliently, not by replacing existing monetary or banking systems, but by streamlining the infrastructure that surrounds them.

Regulatory Landscape

African regulators are approaching digital asset innovation with the same cautious, deliberate posture we see globally. Their focus is on balancing innovation with stability, consumer protection, and the soundness of the financial system.

Key realities:

- Most jurisdictions do not prohibit businesses from using stablecoins for legitimate commercial settlement.

- Regulatory focus is primarily on retail-facing activity, not B2B operations.

- Several markets (including Rwanda, Ghana, Mauritius, and South Africa) have established sandbox programs that allow controlled experimentation.

B2B adoption benefits from this environment. It does not challenge monetary policy transmission or introduce consumer risk. Instead, it supports existing commercial activity, making it a natural place for regulators to allow innovation to proceed. As frameworks mature, this foundation will create space for broader B2C and P2P applications.

Global Implications

Africa’s fragmented monetary landscape makes it an ideal proving ground for digital settlement infrastructure. Technologies that can operate across dozens of currencies, regulatory systems, and capital controls tend to be resilient enough for broader global deployment. While the continent is often highlighted for its complexity, it is worth noting that cross-jurisdictional fragmentation is not unique. Both the European Union and the United States operate within regulatory frameworks that consist of overlapping authorities, divergent state or national interests, and varying compliance requirements.

The challenges differ in scale and form, but the underlying lesson is similar: payment systems must be adaptable to heterogeneous regulatory environments, wherever they emerge.

This aligns with broader shifts in the corporate treasury world:

- Multinationals increasingly treat stablecoins as operational tools.

- Treasury teams value programmability, finality, and 24/7 settlement.

- Global banks are exploring tokenized deposits and integrating digital settlement rails.

Africa’s experience will offer valuable insights for these global developments. Its mix of digital adoption, entrepreneurial energy, and structural friction accelerates the emergence of payment solutions that must prove their value quickly.

From Aquanow’s vantage point, innovations that take root in smaller markets often foreshadow global trends, particularly in environments where fragmented payment systems and cross-border frictions remain challenges.

Looking Ahead

Stablecoin adoption in African B2B markets is poised to accelerate. Businesses are recognizing the operational advantages, while regulators are building frameworks that clarify permissible use. The likely progression is clear:

- B2B cross-border settlement

- Domestic B2B applications where permitted

- Expansion into B2B2C flows

- P2P usage as consumer-facing regulations mature

What is happening in Africa is not merely a regional payment story. Market participants are getting a glimpse into the future of global money movement. The experimentation on the continent is generating practical lessons about digital settlement, regulatory integration, and operational strategy that apply far beyond its borders.

For payments professionals worldwide, Africa represents both an emerging market opportunity and a laboratory for understanding how digital settlement technologies integrate with traditional financial infrastructure. The institutions observing these developments, and building capabilities accordingly, will be best positioned to support the next generation of global commerce.

Next month, The Payment Gap will explore how institutional payment systems are orchestrating stablecoin settlement networks. We’ll examine how banks, fintechs and digital-asset platforms are combining forces to build operational frameworks, manage regulatory and settlement risks, and scale a new “payments layer” without disrupting core banking infrastructure.

.png)