Agentic commerce refers to autonomous software systems that can independently discover needs, research options, negotiate terms, execute transactions, and manage the entire lifecycle of business activities with minimal human oversight. Unlike earlier automation systems that followed rigid, rule-based instructions, these AI agents can interpret intent, adapt to changing circumstances, and make context-aware decisions. Of course, this is all carried out within high-level constraints set by human users.

The distinction becomes clear when comparing today's tech with earlier automation in finance. Traditional robo-advisors follow fixed allocation models based on questionnaires. Modern portfolio agents can analyze your spending patterns, anticipate future expenses, monitor market conditions across asset classes, and dynamically adjust your investments. The critical development that makes this all scalable is that these algorithms can take instructions and explain their reasoning in natural language when asked. OpenAI CEO Sam Altman has described AI agents as “super competent colleagues” that will be able to complete tasks

What makes this possible now? The convergence of three critical technologies: advanced AI reasoning capabilities, programmable financial infrastructure, and secure digital identity systems.

From Language Models to Autonomous Agents

The foundation of agentic commerce rests on recent advances in large language models (LLMs) and agent architectures. Models like GPT-4, Claude, and their successors don’t truly understand or reason in the human sense, but they can simulate reasoning patterns, plan sequences of steps, and generate actions that appear contextually intelligent using probability and pattern recognition.

Financial institutions have already begun deploying these capabilities internally, notably in underwriting. AI systems can now ingest and analyze years of financial statements, credit reports, market data, and alternative data sources in seconds. They help surface key risk factors, highlight inconsistencies, and benchmark applicants against historical patterns across vast datasets. Rather than replacing credit officers or underwriters, these tools augment in-place capabilities by accelerating due diligence, improving consistency, and freeing up human experts to focus on judgment, structuring, and edge case evaluation.

The critical breakthrough came when these models learned to bridge the gap between text and action, translating natural language reasoning into real world outcomes via APIs, databases, and digital services. An investment agent, for example, can now go beyond suggesting a portfolio rebalance to actually executing the trades, recording the rationale, and tracking performance.

This shift, from models that could describe actions to ones that can perform them, marked the moment when theoretical use cases turned into practical tools for finance and commerce. It also reflects their natural role as human augmenters rather than outright replacements. This frees up time, reduces errors, and enhances decision-making rather than removing people from the loop altogether.

Programmable Money and Digital Wallets

Traditional payment systems were designed for human operators. Credit card networks assume a cardholder making deliberate purchases, with fraud detection systems flagging "unusual" activity that diverges from their typical patterns. Bank transfers often require physical signatures or in-person verification. This all constrains what software agents can do independently.

Enter programmable money and digital wallets, the latest financial infrastructure designed for software control:

Major payment networks have begun developing specialized platforms that provide APIs for agent authentication, transaction authorization, and dispute resolution. These systems allow agents to make purchases within carefully defined parameters without requiring human approval for each transaction.

The fundamental challenge involves reimagining the entire payment flow. It's not just about authorizing a transaction, but about encoding permissions, constraints, and accountability into the payment infrastructure itself.

Digital wallets have evolved from simple storage mechanisms to sophisticated financial interfaces with programmable rules. Modern wallets now include delegation controls that let users authorize specific agents to make certain types of purchases up to defined limits and agent permission features that allow granular control over what transactions AI assistants can initiate.

Why Blockchain and Crypto Matter for Agentic Commerce

While traditional financial networks are adapting, blockchain-based systems offer native advantages for agent-based transactions:

First, blockchains are inherently designed for software-controlled assets. Smart contracts (self-executing agreements with terms directly written in code) provide programmable rules that govern how assets can be used, transferred, or transformed. Such architecture is a natural fit for the internet.

Traditional finance assumes humans are the primary actors, with software as a tool. Agentic commerce on blockchains flips this model, assuming software is the primary actor, with humans setting the parameters.

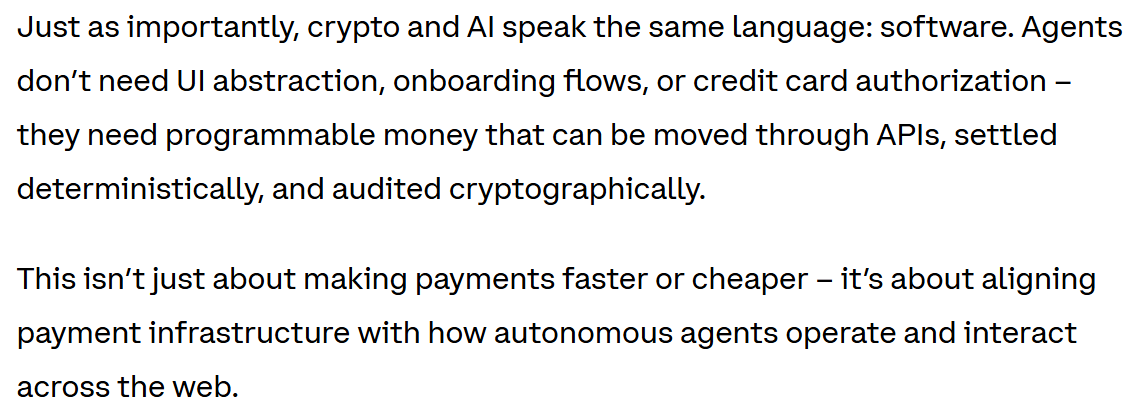

Second, crypto networks enable microtransactions that would be economically unfeasible in traditional systems. When an AI agent needs to pay $0.0001 for a single API call or data point, credit card minimums and percentage-based fees make this impossible. Blockchain-based payment channels can handle such transactions efficiently.

Third, distributed systems are meant to operate continuously without downtime or business hours. Agents don't sleep, and neither should the financial infrastructure they rely on.

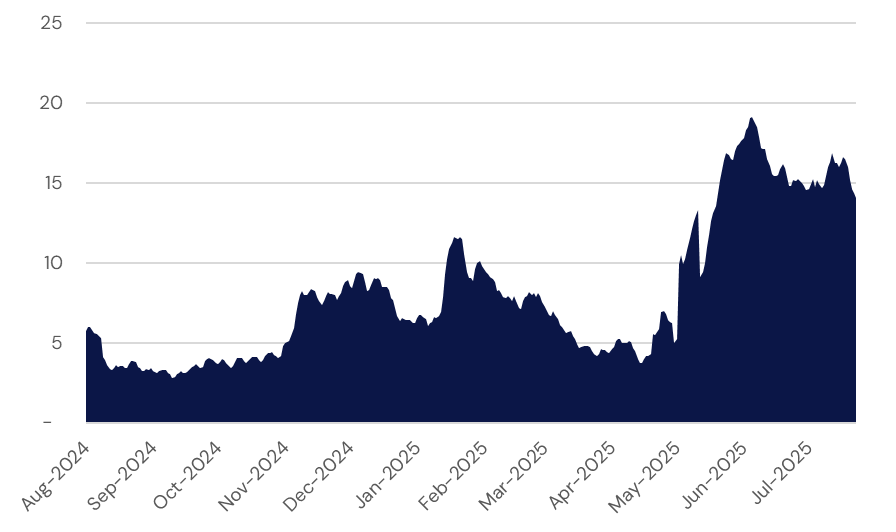

Decentralized exchange protocols demonstrate how financial services can function autonomously through programmable infrastructure. These systems execute billions in daily trading volume with far less human intermediation than traditional structures, using smart contracts to guarantee execution according to predefined rules.

10-Day Average Daily DEX Volume (in billions, USD)

Early Use Cases: From DeFi to Digital Entrepreneurship

Agentic commerce is already transforming several domains. In DeFi, yield optimization protocols deploy capital across lending markets, liquidity pools, and trading strategies to maximize returns. These systems continuously monitor market conditions, rebalance positions, and adjust strategies. They represent autonomous portfolio managers operating 24/7 without human intervention.

In retail, emerging services can automatically reorder household staples when they're running low, negotiating the best price across multiple sellers. Unlike simple subscriptions, these systems make contextual decisions—delaying orders when prices are unusually high or bundling purchases to optimize shipping costs. The changes are happening so fast, that some prominent platforms are beginning to restrict agent activity.

Perhaps most intriguingly, we're seeing the emergence of "" or AI systems that can operate basic business functions with minimal human oversight. These include agents that generate specialized content for niche audiences, publish it across appropriate platforms, monitor engagement, adjust strategy based on performance, and generate revenue through affiliate marketing and subscriptions. The human "owner" simply sets high-level goals and collects profits.

Reshaping Business Economics and Financial Intermediation

The implications for business economics are profound. Agentic commerce fundamentally alters the cost structure of operations by automating not just execution but decision-making itself.

When human involvement is removed from routine commercial tasks, transaction costs drop sharply. This doesn’t just make existing businesses more efficient, it enables entirely new categories of industry that were previously uneconomical.

For example, a small business might not be able to afford a full-time finance team to manage hundreds of vendor invoices, reconcile contracts, track delivery terms, and execute payments. An AI agent can handle the bulk of that work automatically by flagging discrepancies, enforcing terms, and processing payments, while freeing up time for human staff to focus on higher-leverage activities like sales or marketing.

For financial institutions, the emergence of agentic commerce introduces both opportunity and constraint. While traditional intermediaries risk being bypassed in agent-to-agent transactions, the more immediate tension lies in the gap between what is technically possible and what is regulatorily permissible.

Fintechs, with lighter compliance burdens and faster iteration cycles, are better positioned to explore agent-driven workflows. They can deploy AI in underwriting, customer support, or transaction processing with relatively few barriers. In contrast, banks operate under stricter regulatory oversight, so there is little appetite for autonomous agents acting without clear controls.

That is why much of the early experimentation is happening on crypto-native platforms. Blockchains are already optimized for programmable money, run continuously, and offer the composability agents require. In the current political environment, the industry appears to be enjoying a sort of regulatory safe harbor, making it a natural testing ground for agentic commerce.

Forward-thinking institutions are already adapting, offering specialized APIs, compliance rails, and risk tooling tailored to autonomous systems. The strategic shift is subtle but significant, moving from executing transactions to enabling autonomous financial activity.

Navigating Risks and Regulatory Questions

The rise of agentic commerce brings significant opportunities, but it also surfaces real challenges. As autonomous systems take on more responsibility, new forms of fraud and exploitation become possible. Malicious actors can deploy their own agents to manipulate platforms, target vulnerabilities, or automate illicit activity at scale.

Regulatory frameworks built around human decision-makers are ill-equipped to handle this shift. When an AI agent makes an unauthorized purchase or violates financial regulations, who is responsible? Is it the developer, the user, or the platform that enabled it? These questions remain largely unanswered, and regulators are still working to define accountability in an agent-driven environment.

Privacy concerns also come into sharper focus. Agents that manage day-to-day activity can generate detailed behavioral profiles, combining transaction data, preferences, and patterns in ways few human actors ever could.

These are not minor headwinds. Because of them, I expect broad rollouts of agents for consumer use to remain limited for the time being. Instead, early growth is likely to continue in areas where agents already have traction: DIY use cases, small-scale business tasks, crypto ecosystems, and internal tools within larger institutions focused on efficiency gains rather than public-facing autonomy.

Markets of Agents and New Economic Paradigms

Looking ahead, we can glimpse a future where agents don't just serve individual humans but interact with each other in complex economic ecosystems.

Imagine a marketplace where your personal shopping agent negotiates with seller agents, logistics agents coordinate delivery, and financial agents manage payments and dispute resolution, all without human intervention until final approval or in exceptional circumstances.

For investors and builders, this shift represents perhaps the most significant opportunity since the early internet. Just as the web transformed information exchange, agentic commerce is transforming economic exchange itself.

The financial institutions that thrive will be those that position themselves as the trusted infrastructure for this new paradigm, providing the identity systems, payment rails, risk management tools, and regulatory compliance frameworks that agents require.

The financial services industry is pivoting from building services for humans using software to building services for software that serves humans. The age of agentic commerce has begun, and with it, a fundamental reimagining of how economic activity unfolds in the digital age.