Are you sick of reading about Bitcoin ETFs? Good news! That isn’t the topic of this week’s Digital Dives (even if the initial response has been staggering). However, I do think we can learn about the future by stepping back and appreciating how far the crypto sphere has come. Today, some of finance’s most prominent investment houses are sponsors to funds whose underlying asset didn’t even exist two decades ago. Since that time, many of the world’s most powerful executives and policymakers have pivoted their stance from abject disapproval to a more receptive and accepting engagement. Many now assert that blockchains will underpin the customer relationships and transactions that fuel the global economy.

Back in 2009, the crypto ecosystem had effectively no overlap with the mainstream economy. As Bitcoin gained more traction, other cryptocurrencies and blockchain projects started to emerge, each offering unique features and use cases. This diversification helped to attract a wider range of participants, from individual investors and developers to startups and large corporations. The narrative began to change from Bitcoin as an obscure digital currency to a legitimate asset class and a groundbreaking technology with far-reaching implications. Naturally, as the community of crypto supporters grew, financial services like trading, research, and fiat on-/off-ramps became necessary.

In the early days it was easy for regulators to ignore Bitcoin. But, as its usage and value began to expand, colliding increasingly with the traditional financial system, suddenly policymakers felt the need to act. Frankly, it’s a good thing they did because the incidence of grift and fraud was getting carried away and remains a headwind to broader adoption today. However, following several high-profile debacles that made victims of some of the savviest investors, the world’s financial watchdogs have begun to enact comprehensive legal frameworks for the burgeoning crypto economy.

The European Union's finance ombudsman recently proposed to expand its stress testing to Non-Bank Financial Intermediaries, including stablecoin issuers. The move comes in response to greater interconnectivity between banks and other operators. Among the recommendations is that issuers of stablecoins backed by fiat have sufficient liquidity for full redemption. This move, aimed at enhancing investor protection, implies a significant and growing prominence of stablecoins in the digital economy. Major issuers, including PayPal, are already in compliance, showcasing a proactive stance towards regulatory adherence.

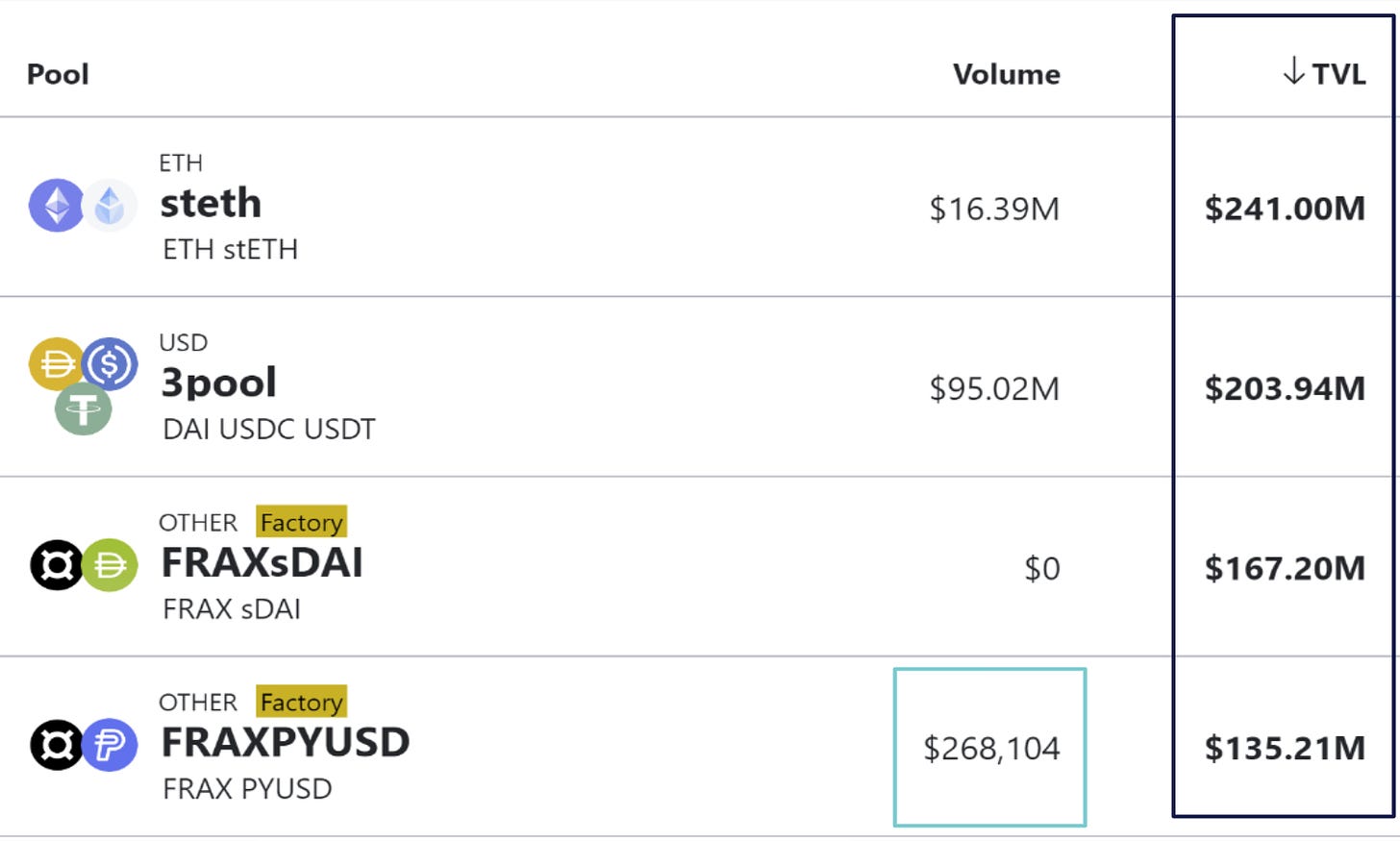

Sticking with the theme of converging markets, PayPal's PYUSD, is now a component of Curve Finance's fourth largest vault. The PYUSD-FRAX liquidity pool, has $135M in TVL but paltry volumes of $270K*. What’s interesting is that it’s comprised of regulated fiat-backed and unregulated crypto-collateralized stablecoins. While the volumes leave something to be desired, this is effectively a bridge between PayPal’s gated crypto environment and decentralized finance. That said, the regulatory implications here are interesting. The EU’s Markets in Crypto-Assets (MiCA) does not currently extend to DeFi, which might encourage further innovation in the stablecoin sector there. Meanwhile, regulation by enforcement in the U.S. is much more confusing and this is the jurisdiction of importance for PYUSD. Things could get awkward.

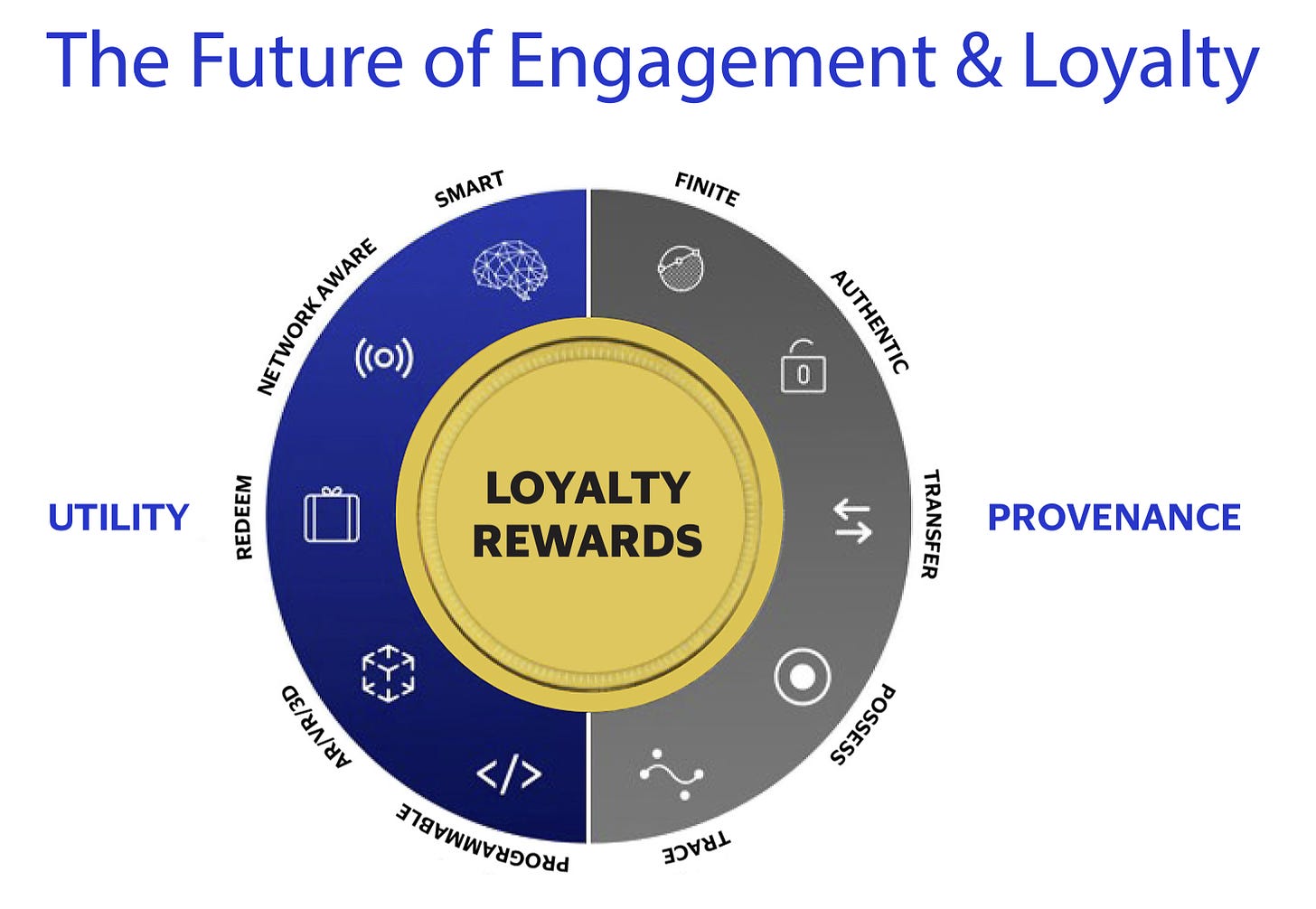

Crypto rails are purpose built for the digital age, making tokens (particularly stablecoins) better stores of value and mediums of exchange than the private ledger updates and correspondent banking transfers of traditional networks (on-/off-ramps notwithstanding). This helps explain why credit card network providers have been among the most consistently engaged with blockchains. Visa recently expanded its stablecoin settlement capabilities to the high-performing Solana blockchain. Through live pilots with issuers and acquirers, Visa has already moved millions of USDC between its partners over the Solana and Ethereum blockchain networks to settle fiat-denominated payments. During the holidays, Visa demonstrated that they've caught on to the diversity of digital assets beyond payments. Web3 Loyalty Engagement Solution enables brands to create digital wallets for storing reward points and experiences, marking a significant move towards leveraging digital ownership rights to foster deeper client relationships. This initiative is part of a growing trend among brands to embrace blockchain technology for enhanced customer engagement.

One of the more interesting examples of traditional and crypto markets moving closer together can actually be illustrated through a divergence. Towards the end of December, TradFi traders at the CME showed a bias to close long positions, while their counterparts on crypto-specific venues continued to add leverage via perpetual swaps. The effect was that the premium paid to own futures on the Chicago board nearly disappeared, while traders were paying significant funding rates to express levered long positions elsewhere. This situation culminated with a 5% market correction, that wiped out nearly $600M of long positions on crypto exchanges. These are powerful signals in the world of investing where “alpha” is the most sought-after commodity (after fees, I suppose). Those keeping an eye on both markets may have noticed the risk aversion on the CME, reducing their exposure to protect against losses or even going short to capitalize on a sharp reversal in price trend.

We can now trade spot BTC ETFs, which will soon have listed option contracts. It’s likely that there will be differences between the implied volatility surfaces across traditional and DeFi venues, providing insights into the trading segments’ outlook. Perhaps more importantly, arbitrage/relative value opportunities will be present for those who can participate across exchanges. Could jurisdictional regulatory differences create a moat around these profits? Capital is like water, so I suspect the associated flows will erode the frictions, further connecting the traditional and decentralized financial ecosystems.

Last week, Larry Fink (a former crypto skeptic) highlighted that “ETFs are step one in the technological revolution in the financial markets… Step two is going to be the tokenization of every financial asset.” This perspective supports the narrative of unwavering integration between blockchain technology and finance. Bridging the gap between the current situation and widespread crypto adoption remains a significant challenge, but in the context of how far we’ve come in only 15 years, it’s easy to be optimistic.

The continued overlap between traditional financial institutions, established brands, and crypto-native platforms is undeniable. This convergence is fostering a landscape ripe with both opportunities and challenges. As this integration progresses, it's crucial to operate with a keen understanding of the complexities involved. The future of finance is being reimagined, weaving together the established relationships and processes of traditional finance with the dynamic innovation and adaptability of the crypto economy.

Aquanow specializes in unlocking digital asset potential for financial institutions. Contact us to explore how our expertise can enhance your performance.

If you want to contribute to the web3 movement, Aquanow is on the look for curious and motivated folks to join our team. Feel free to reach out directly or check out the current openings here.