Central bankers are adopting a less hawkish tone as softer data suggests the economy is no longer overheating. This has resulted in yields coming in marginally from levels not seen in decades, buoying the prices of riskier investments in anticipation of a goldilocks economy. Some assets like Gold and Bitcoin have been bid-up on the prospect of loose monetary policy to follow. Riding those narratives, a low liquidity environment, and some idiosyncratic catalysts, the digital asset markets are enjoying a period of relative strength.

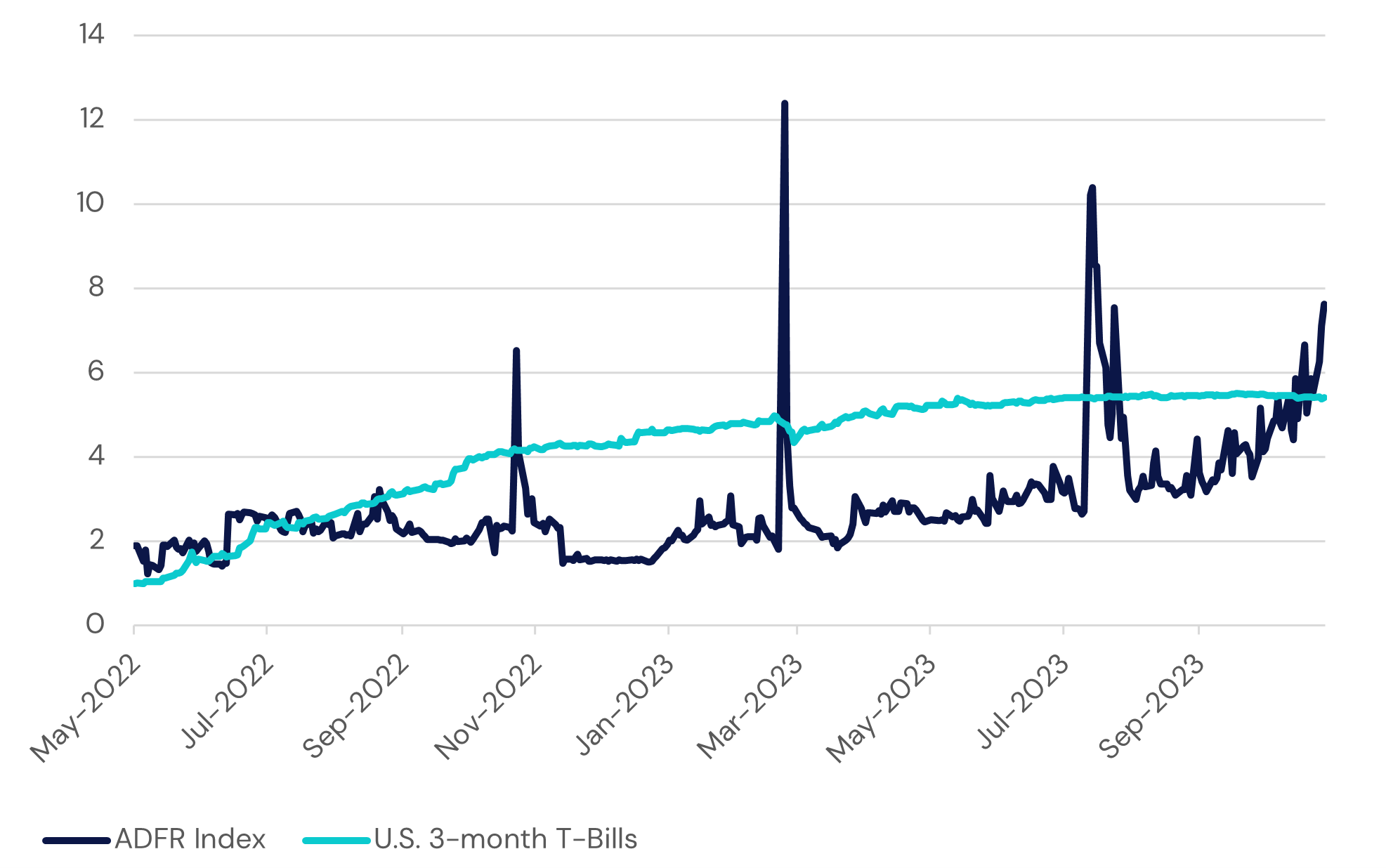

Observers of both traditional and crypto markets have noted a significant trend reversal recently. While it’s nice to see token prices recovering some of their cyclical losses, this isn’t the dynamic I’m referring to. As benchmark yields like U.S. Treasuries have subsided, lending rates in DeFi have moved higher, and for the first time in 18 months, the Aquanow DeFi Funding Rate (ADFR) has rested above the U.S. 3-month Treasury yield for weeks.

ADFR and 3-month U.S. Treasury Bill Yield (in percent)

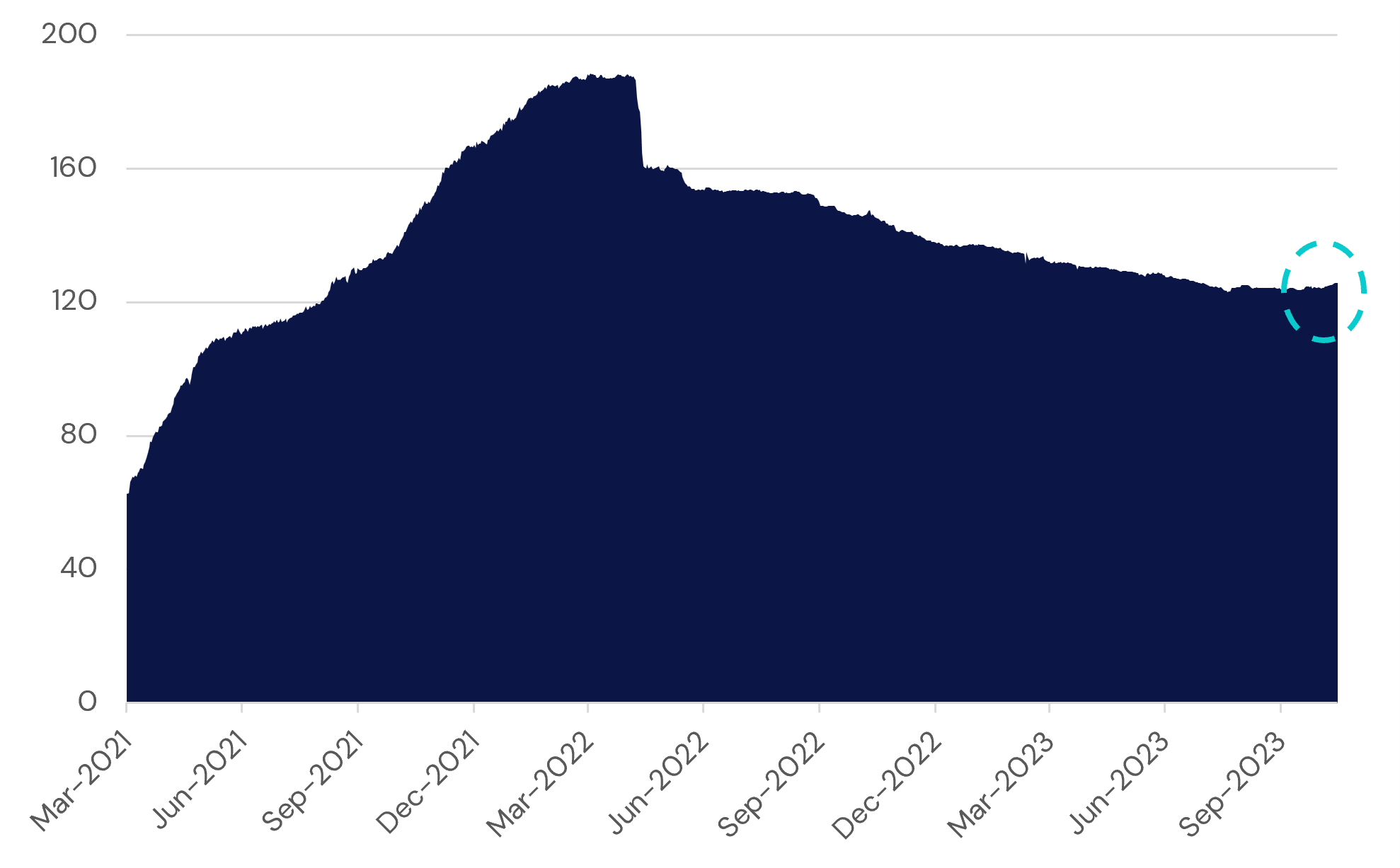

The blockchain economy once offering lower capital costs than even the most liquid global markets has perplexed many. If you can earn more by lending to the U.S. Government than some crypto trader, you should do so all day. Let alone the notion that, in the latter, you’re trusting a smart contract whose code has been audited but could still be susceptible to exploit. Reacting to these dynamics, a steady 18-month decline in stablecoin supply signaled capital's shift to more lucrative off-chain opportunities. However, it’s likely that some of the funds in the ecosystem were somewhat “trapped” due to investment mandate, philosophy, or on-/off-ramp frictions. This had the effect of supressing lending rates as capital went to the safest places it could earn something and avoid the contagion. Importantly, the market cap of stablecoins recently broke its downtrend. Are investors returning to seek higher returns in crypto?

Total Stablecoin Market Cap (in billions, USD)

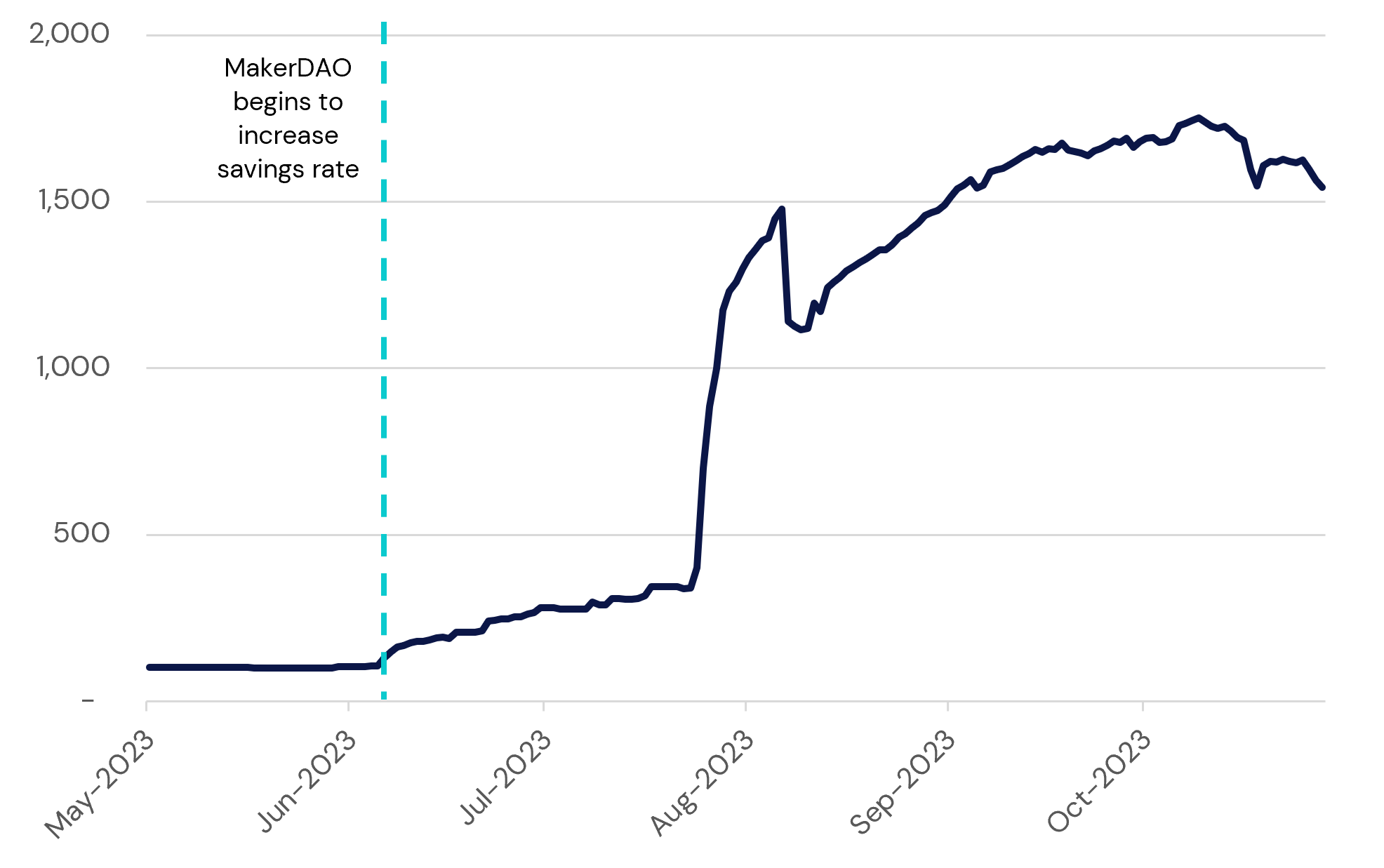

This summer, the DeFi economy saw a pivotal shift with MakerDAO's DAI Savings Rate (DSR) increase from 1.0% to a peak of 8% (now 5%), marking a notable change in the stablecoin yield landscape. As a non-fiat backed asset, the decentralized stablecoin isn’t for everyone. However, Maker was suddenly paying 2.25x more on balances than what investors could earn by lending through protocols like Aave or Compound, so naturally, capital flowed to the DSR. You can scroll up to the first graph to see how this coincides with and inflection of the ADFR (after a spike driven by concerns at Curve).

Capital Committed to the DSR Module (in millions, USD)

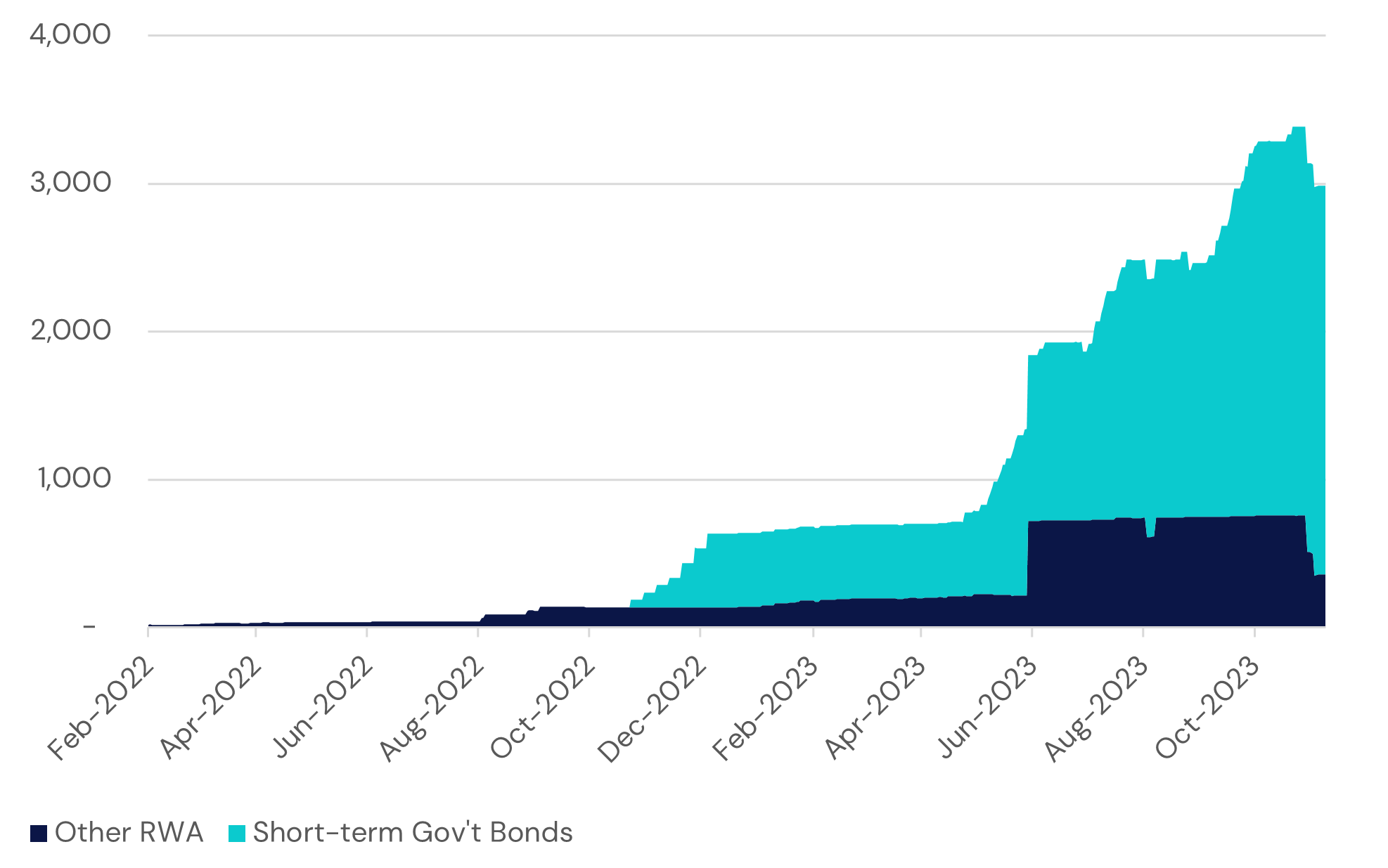

The sustainability of the higher disbursement was enabled through the tokenization of real-world assets. Maker added $2.6B in U.S. Treasuries as DAI collateral this year, advancing their RWA experimentation. This has meaningfully impacted the group’s profitability, contributing over $11M of monthly revenue. The borders between the digital asset and mainstream economies are beginning to blur and the results are fascinating.

MakerDAO Real-world Asset Collateral (in millions, USD)

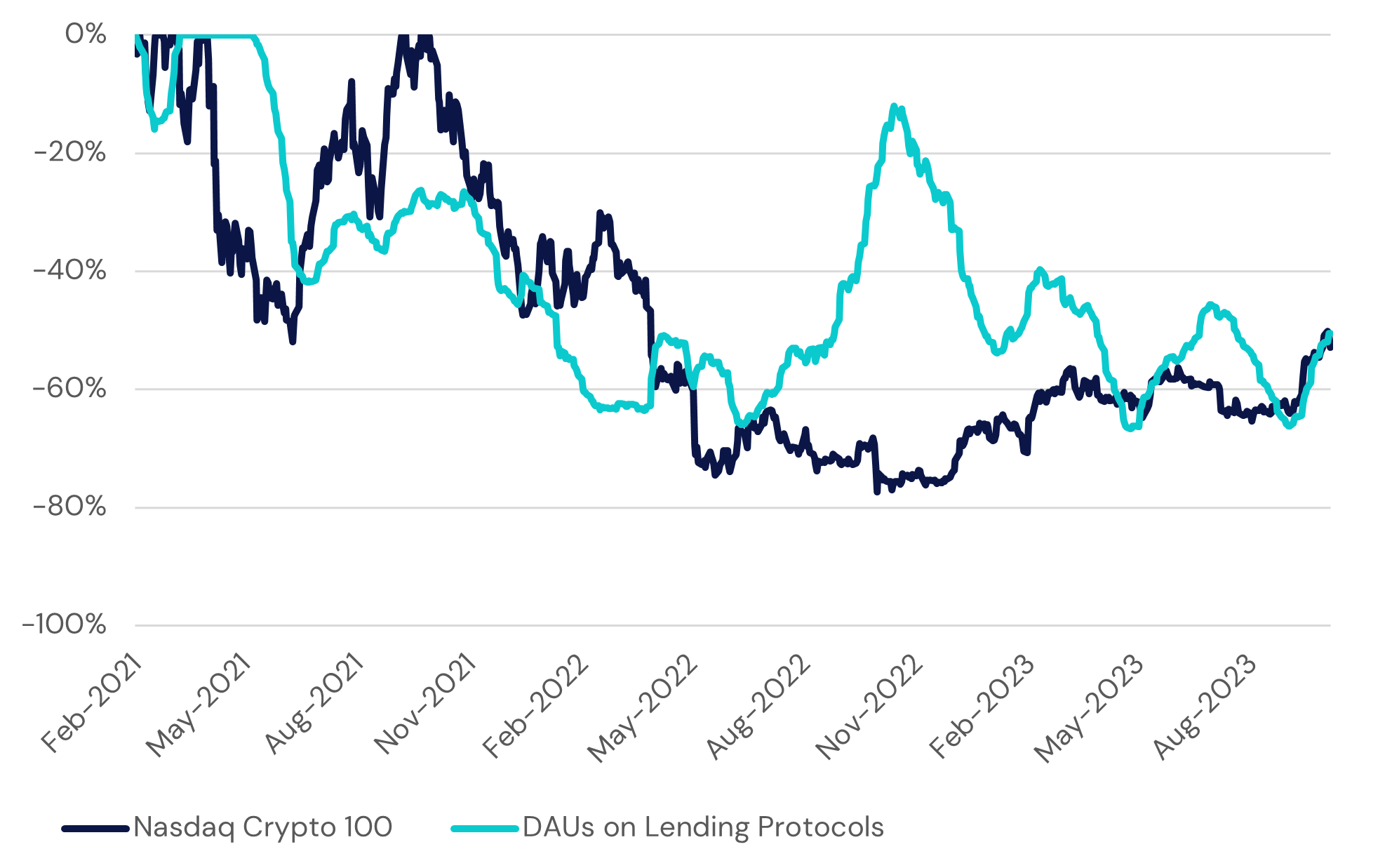

Despite stellar year-to-date performance, digital asset prices remain meaningfully below their peaks. Similarly, on-chain lending activity has seen a nice rebound, but pales in comparison to the exuberance of the last bull market. Crypto native credit venues were only launched during the last cycle. The valuation losses and code exploits of the past couple years have been a setback for digital asset adoption. That said, the technology of the major lending protocols has withstood the pressure of the 2022 collapse. It’s been intriguing to see these markets operate (mostly) without fail as considerable amounts of leverage was washed out of the system.

Price and Daily Active User (DAU) Drawdowns from Peak Levels

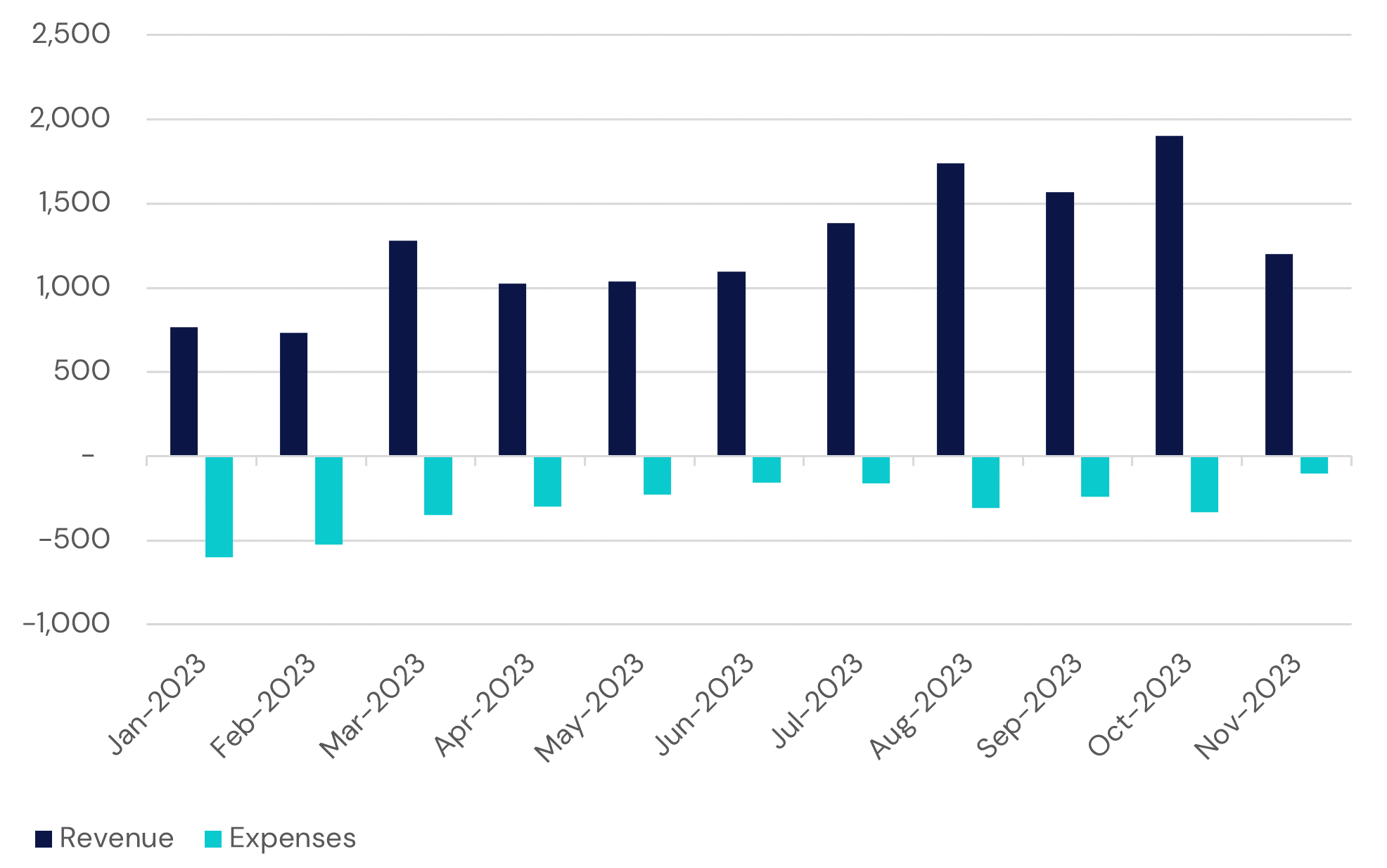

We’ll see if token prices and activity can sustain their current momentum, marking the beginning of a new cycle, but for now optimism is abound. This means that speculators will increasingly look to protocols like Aave to take on leverage. This has the effect of increasing rates of return in DeFi lending, which is welcome news for those who stuck through the period when rates on short term government debt offered far more attractive returns. It is also good news for the treasuries of the related projects. Aave has seen a nice increase in profits recently.

Aave Monthly Revenues and Expenses (in thousands, USD)

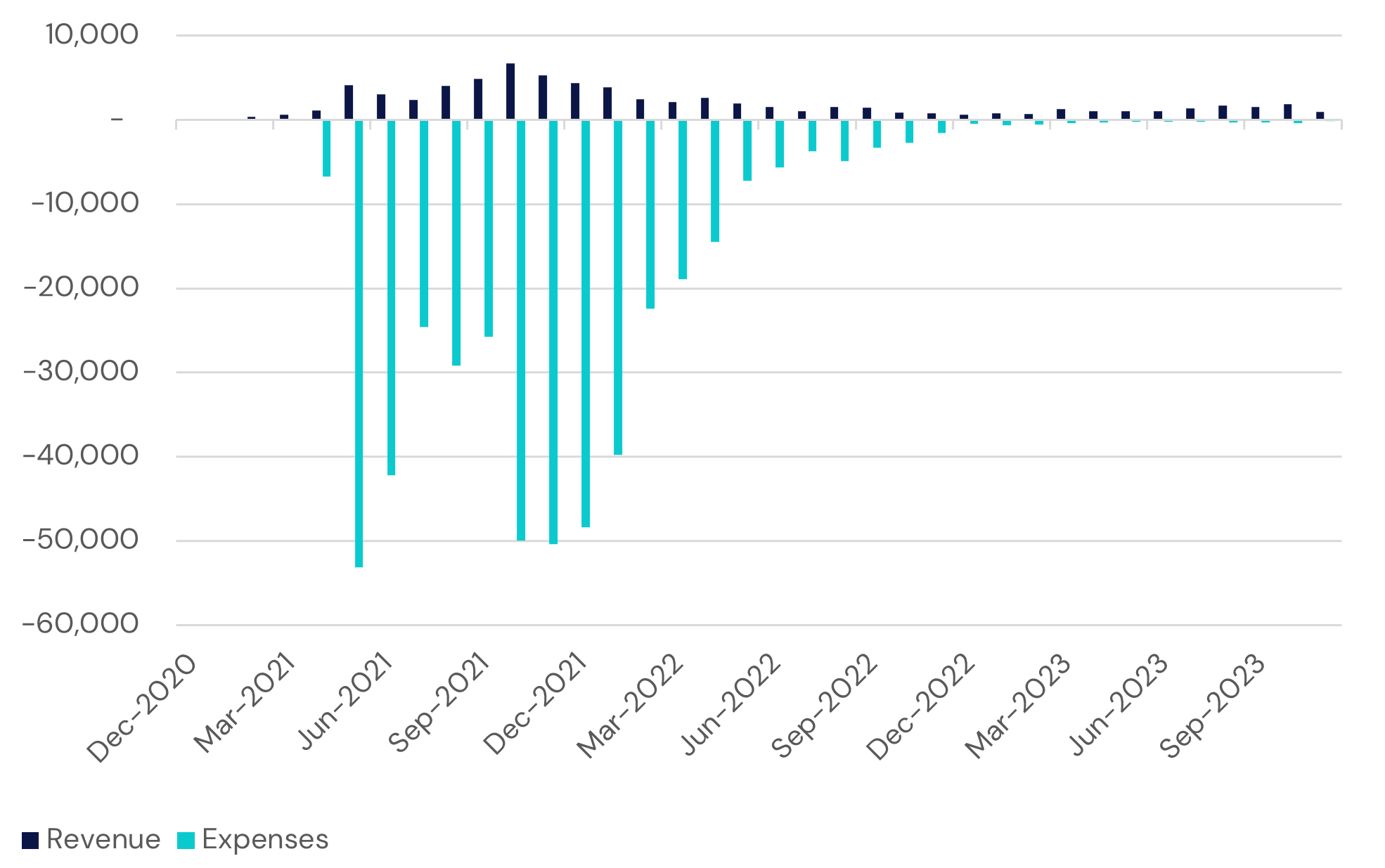

Something I’ve been thinking about, is the idea that the established products of the past cycle have found some degree of market fit and they’re ready to accept new and returning traders. In 2020, Compound kicked off DeFi Summer by introducing yield farming or paying users to interact with its money markets. Seeing how this stimulated activity, most others followed suit. Below you can see how the cost of token incentives compared to Aave’s revenue over the same period.

Aave Monthly Revenues and Expenses/Token Issuance (in thousands, USD)

Conceivably, the projects which have lasted through the cycle won’t have to incentivize users to the same extent (or at all) this time around. This means a group like Aave stands to bring in $50M+ in annual revenue, which is meaningful for a project sporting a fully diluted valuation of $1.4B and whose run rate expenses are estimated at $5M, indicating a P/E of about 30x or less. How this value eventually accrues to tokenholders remains to be seen. Securities laws remain dynamic and preclude some common avenues to disburse capital. Further, we’re still very early in finance’s digitization and teams like Aave’s have proven themselves capable of continued innovation, so perhaps the best course of action is to reinvest and continue building. The open-source nature of the industry is also a consideration here, but we’ve seen players erect temporary barriers in the past, which might help sustain moats if network effects can be sufficiently entrenched.

The recent surpassing of traditional benchmarks like U.S. Treasuries by DeFi yields signifies a pivotal shift, potentially highlighting the maturation of the crypto ecosystem. Integrating real-world assets into DeFi platforms, exemplified by MakerDAO's use of U.S. Treasuries, marks a significant stride in blending traditional and digital finance. Despite challenges such as market volatility and regulatory uncertainties, major DeFi protocols have demonstrated resilience, suggesting a promising future for this sector. As we anticipate a new cycle of digital asset engagement, established projects like Aave are well-positioned to capitalize on this momentum, moving towards more sustainable revenue models. The ongoing convergence of financial marketplaces presents a transformative opportunity set, with immense potential for innovation and growth.

Aquanow specializes in unlocking digital asset potential for financial institutions. Contact us to explore how our expertise can enhance your performance.

If you want to contribute to the web3 movement, Aquanow is on the look for curious and motivated folks to join our team. Feel free to reach out directly or check out the current openings here.