.png)

How Stablecoins Are Winning Where Traditional Networks Fail

When incumbent payment giants begin dropping billions of dollars to acquire their stablecoin challengers, the industry has moved past the proof of concept phase. In March 2026, Mastercard announced a blockbuster $1.8 billion deal to buy London-based stablecoin infrastructure firm BVNK. This followed after Stripe’s $1.1 billion acquisition of the stablecoin platform Bridge in October 2024. These deals send a clear message: stablecoin payment adoption has finally “crossed the chasm” from early adopters to mainstream finance.

The motivation for these global financial institutions is clear. Conventional rails are increasingly too sluggish, expensive, and structurally flawed for the modern digital economy.

Systemic Friction in Legacy Rails

While a credit card authorization feels instantaneous to a consumer, the settlement takes 1-3 business days to go through issuing banks, acquiring banks, and clearinghouses. It is also costly: credit card interchange fees typically range from 1.5% to 3.5%, plus a fixed swipe fee of around $0.30 to $0.50 per transaction.

When transactions cross borders, time and cost multiply. International wire transfers rely on the legacy SWIFT network of correspondent banks. This system forces funds to sit in transit for 2-5 business days and incurs high FX spreads and intermediary deductions around 6.5%, trapping an estimated $120 billion in liquidity annually.

This patchwork system also creates a barrier to access. Because a transfer must pass through multiple intermediaries, each with its own varying risk appetite and compliance framework, the final outcome is the strictest combination of all those standards. If even one bank or network in the chain deems a specific region, transaction size, or business model too risky, the entire payment is blocked.

Given the frictions in time, cost and compliance, here are three specific use cases that are the most promising frontiers for stablecoin disruption:

Agentic Commerce: Money for the Machine Economy

AI agents are a completely new class of economic participants. While no humans can (or want to) authorize 1,000 API calls per hour or pay for 100 news articles every single time, AI agents are designed to handle these high-frequency, pay-as-you-go services with ease. However, they are currently throttled by the payment fee structures (such as a $0.3 fixed fee on top of a 2-3% interchange rate on credit cards) that make micro-payments infeasible. Moreover, traditional consumer protection like chargebacks are incompatible with digital machine commerce: it simply doesn’t work to offer chargeback protection for a $0.003 API call after the dataset has already been consumed by the buyer.

Stablecoins based on high-performance networks bypass these bottlenecks. A recent example is the Tempo blockchain launched by Stripe and Paradigm in March 2026. Built for stablecoin payments and automated commerce, Tempo eliminates unpredictable crypto gas fees, targeting a cost of less than $0.001 per transfer that can be paid in the same stablecoins. Because blockchain transactions are irreversible, the risk of chargebacks is eliminated for the seller.

Supporting this is the Machine Payments Protocol (MPP), an open standard that is basically "OAuth for money". MPP allows AI agents to authorize a pre-set budget, enabling them to stream thousands of micro-payments for data or API calls. These are aggregated into a single settlement, making true pay-per-use commerce viable at scale.

B2B Payments: Unlocking Trapped Capital

For multinational companies, B2B payments to suppliers and partners have always been an expensive headache of trapped capital and pre-funding requirements. While the traditional financial industry has attempted to optimize SWIFT through efforts such as SWIFT gpi (Global Payments Innovation) and ISO 20022, the actual monetary settlement remains to be a few days. Because networks like SWIFT only transmit payment instructions, actual monetary settlement still takes days because funds must pass through intermediary banks that do not operate on weekends and require manual AML checks. This forces institutions to lock up massive amounts of capital in pre-funded nostro accounts in various markets just to execute same-day transfers.

Stablecoins transform this process by settling in seconds or minutes, regardless of jurisdiction or holidays. This eliminates the multi-day "float" and the need for large amounts of local currency reserves. It is no surprise that B2B payments currently dominate real-world stablecoin utility, capturing a massive share of the billions in genuine payment volume.

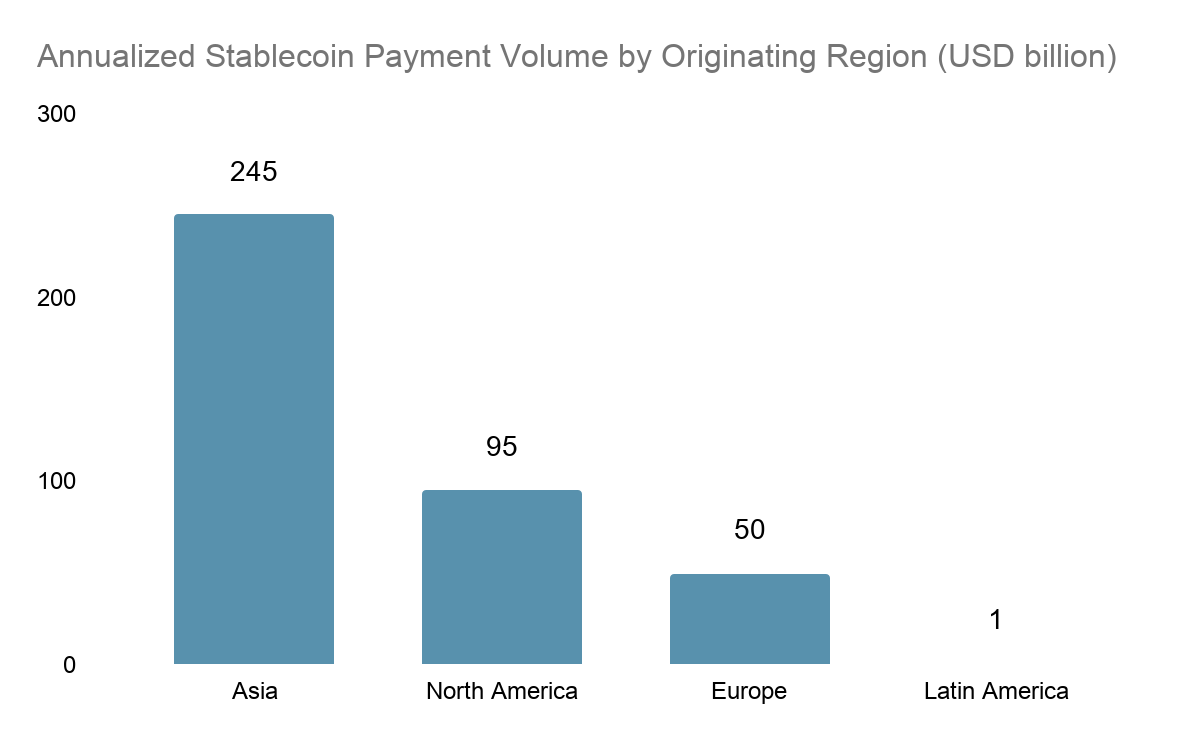

Interestingly, this B2B volume is heavily concentrated in Asia. According to McKinsey, payments originating from Asia represent the largest source of stablecoin volume globally. This flow is driven almost entirely by corporate and institutional activity in financial hubs like Singapore, Hong Kong, and Japan, accounting for about $245 billion in payments, or 60 percent of the total. The dominance is likely due to volatile local currencies (especially across China and Southeast Asia), proactive regulators, and lack of direct correspondent banks for USD.

For corporate treasurers, stablecoins are a pure working capital optimization strategy. Money once trapped in transit can now be freed to generate yield, and to be deployed the moment an invoice is settled.

Gig Economy: Solving the Payout Bottleneck

As the workforce becomes borderless, legacy payout systems have become a significant hurdle for global platforms. Cross-border payroll and remittances currently account for approximately $90 billion in annualized stablecoin volume.

For a platform that pays thousands of gig workers in tens of jurisdictions, sending payouts through the traditional bank network is both slow and costly. By the time a payment navigates through all the banks to be eaten up by FX markups and transfer fees, the final payout can shrink by as much as 10% and take days to settle.

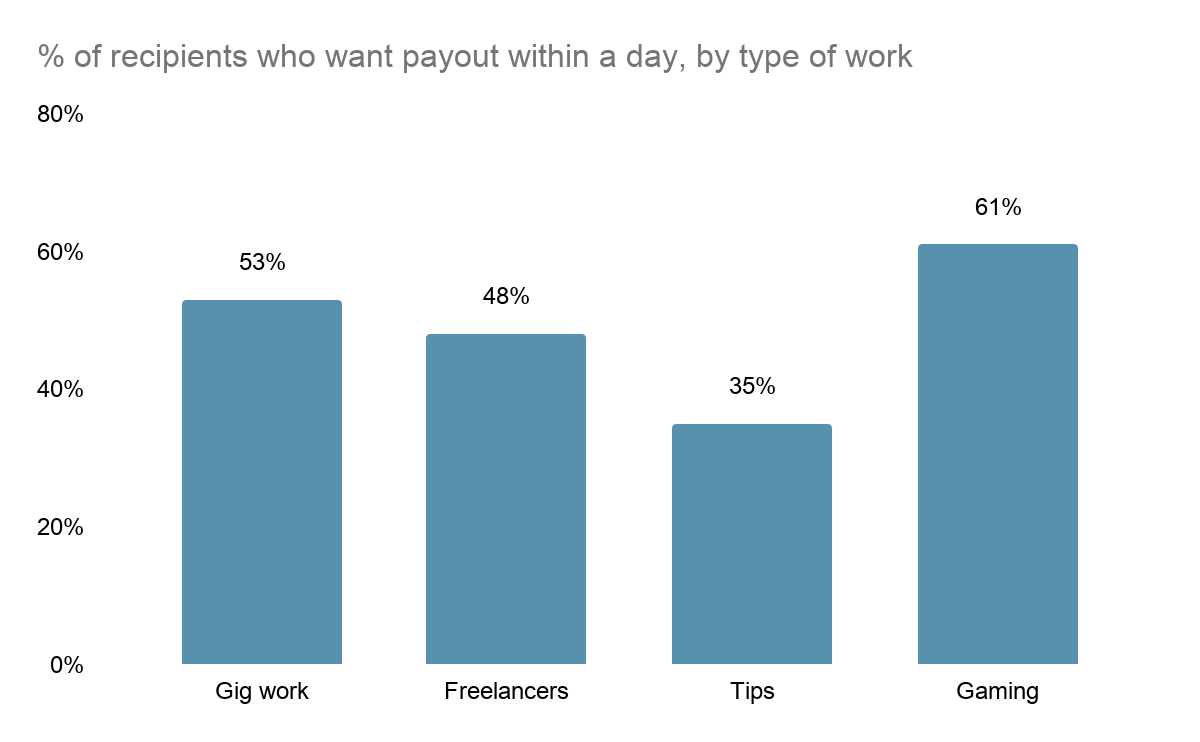

While cost reduction is a clear benefit, the primary driver for adoption has shifted toward liquidity and instant access. According to a Visa report, payment delays are the leading operational pain point for digital entrepreneurs, with 30% of creators specifically demanding features that provide immediate access to earned funds to maintain their business momentum. This is echoed by PYMNTS Intelligence data from late 2025, which indicates that 54% of gig workers want to be paid within a day after the payouts have been issued. Stablecoins solve this by settling in seconds, effectively turning payroll into an on-demand service. This is most visible in the "stablecoin sandwich" model used in the US-Mexico corridor, where providers move value across borders via stablecoins and settle to the recipient in Mexican pesos via local instant payment networks. This architecture allows users to benefit from blockchain’s real-time speed and USD-pegged stability without touching crypto.

The Regulatory Green Light

For years, the primary barrier to enterprise stablecoin adoption was not technological, but regulatory. Corporate treasurers and institutional providers could not justify migrating to infrastructure that existed in a legal gray area. By 2026, however, those barriers have largely been dismantled.

The final piece of the puzzle arrived in March 2026, when the SEC and CFTC issued landmark joint guidance officially classifying major digital assets as "digital commodities." This followed a global wave of legislative clarity, including the U.S. GENIUS Act, the EU’s MiCA framework, and rigorous new licensing regimes in Japan, Singapore, and Hong Kong. By establishing clear standards for reserve backing and parity redemption, regulators have effectively ended a decade of legal ambiguity, allowing banks to hold and process stablecoins with institutional confidence. This regulated environment is the true catalyst behind recent multi-billion-dollar acquisitions by giants like Mastercard and Stripe. These institutions recognize that while traditional consumer checkouts are largely a solved problem, a new era of high-velocity, borderless commerce is emerging. From autonomous agentic payments to B2B treasury optimization, stablecoins have evolved into the new global standard for value transfer.

References and Sources:

McKinsey & Company. Stablecoins in payments: What the raw transaction numbers miss. 2026.

Visa. Monetized: Visa 2025 Creator Report. 2025.